Semiconductor Giants and Market Dynamics: From Storage Rally to SpaceX's Bond Selloff

Keywords: Semiconductor, Storage, SpaceX, Elon Musk, Market Trends, Western Digital, Seagate, Bond Selloff

Introduction

The global semiconductor landscape has witnessed a series of divergent movements in recent weeks, reflecting both robust demand in certain segments and heightened uncertainty in others. While storage giants like Seagate and Western Digital have enjoyed a notable rally in share prices, SpaceX—a company often associated with cutting-edge chip usage in aerospace—has experienced a significant bond selloff following a major move by Elon Musk. This article delves into these contrasting trends, examines their underlying drivers, and offers insights into what they signal for the broader semiconductor and technology markets. The visual evidence from market data further illuminates these developments.

The Storage Sector Surge: Seagate and Western Digital Lead the Rally

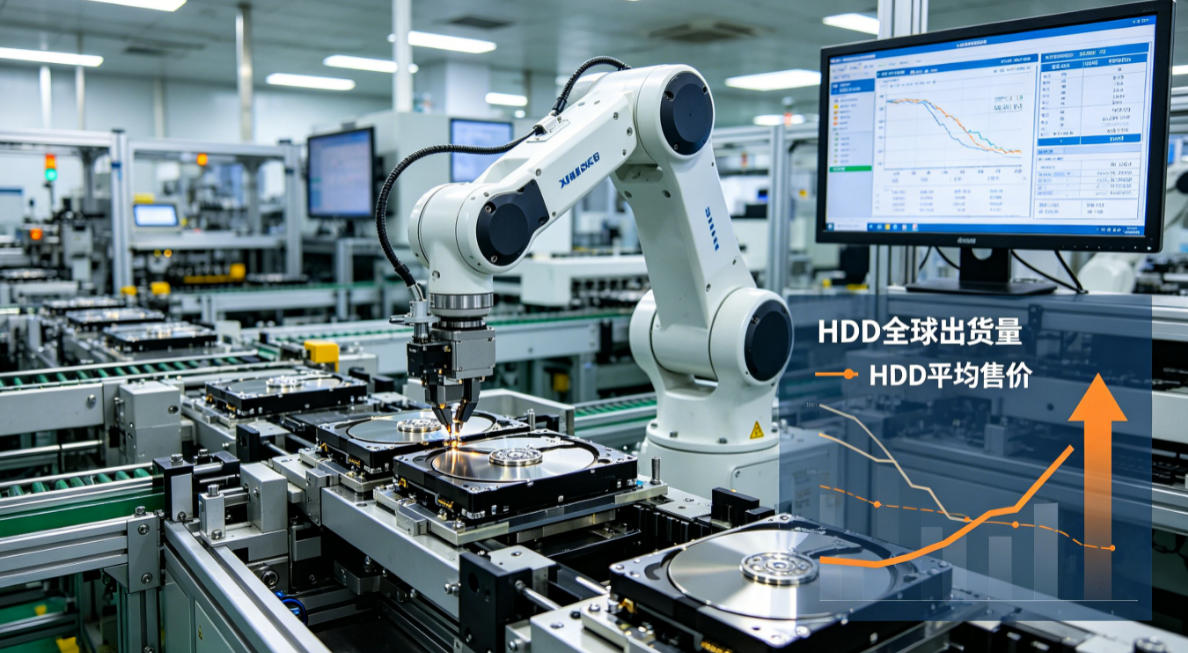

The first notable trend comes from the data storage segment, where Seagate Technology and Western Digital have posted impressive share price gains. As depicted in the chart below, both companies have seen a clear upward trajectory, reflecting strong investor confidence amid rising demand for high-capacity storage solutions driven by cloud computing, artificial intelligence, and data center expansion.

This rally is not accidental. The global shift toward AI workloads and large-scale data analytics has created an insatiable appetite for hard disk drives (HDDs) and solid-state drives (SSDs). Seagate, in particular, has leveraged its advanced heat-assisted magnetic recording (HAMR) technology to deliver higher density drives, capturing a significant portion of enterprise contracts. Western Digital, meanwhile, has benefited from its dual product portfolio spanning both HDDs and NAND flash, allowing it to serve a wide range of end markets.

Analysts attribute the recent price surge to several catalysts: improved supply chain conditions, stabilizing NAND prices after a prolonged downturn, and forward guidance that exceeded consensus estimates. More importantly, the storage rally underscores the cyclical nature of the semiconductor industry—down cycles eventually give way to upcycles, and those who position themselves early reap the rewards. For investors, the chart tells a story of momentum fueled by fundamental strength, not merely speculative trading.

SpaceX Bond Selloff: A Contrasting Signal from the Aerospace Frontier

While storage stocks soared, a different narrative unfolded in the bond market for SpaceX. The company’s debt securities experienced a notable selloff, coinciding with Elon Musk’s major strategic move—details of which remain under scrutiny. The cover image below highlights the headline that captured market attention.

The selloff appears to stem from a combination of factors. First, Musk’s decision to reallocate resources toward his other ventures, including X (formerly Twitter) and xAI, raised concerns about capital discipline at SpaceX. Bondholders, who prioritize predictable cash flows and strategic focus, reacted negatively to the perceived distraction. Second, rising interest rates in the broader economy have made riskier debt instruments less attractive, pressuring yields on SpaceX bonds upward. Third, the company’s heavy reliance on government contracts and its ambitious Starship program—while revolutionary—carry execution risks that may have been discounted in the current environment.

It is worth noting that the bond selloff does not necessarily imply a deterioration of SpaceX’s core business. The company continues to dominate the commercial launch market and has a robust order backlog. However, the episode highlights the sensitivity of capital markets to leadership actions and strategic pivots, especially for companies that operate in capital-intensive sectors with long development cycles.

Connecting the Dots: Implications for the Semiconductor Ecosystem

Though appearing unrelated, the storage rally and the SpaceX bond selloff both reflect deeper currents in the semiconductor value chain. Seagate and Western Digital are direct beneficiaries of silicon demand—their storage products incorporate controllers, memory chips, and other semiconductor components. The rally suggests that end-market demand for these chips is healthy, reinforcing the broader semiconductor upcycle narrative.

On the other hand, SpaceX is a major consumer of specialty semiconductors for its satellites, rockets, and ground equipment. A slowdown in its capital spending—if triggered by the bond selloff or Musk’s strategic reset—could dampen orders for certain high-reliability chips. But this effect is likely localized. The aerospace segment represents a small fraction of total semiconductor demand compared to cloud computing and mobile devices.

From an investment perspective, the divergence offers a lesson: not all segments move in unison. The ability to identify subsectors with strong structural tailwinds, such as data storage amid AI growth, can yield superior returns even when broader market sentiment is mixed. The SpaceX episode serves as a reminder